Problem: manual monitoring is inefficient

Funding rates change every 8 hours (or more frequently depending on the exchange). Monitoring spreads across 9+ exchanges for hundreds of pairs manually is physically impossible. Opportunities appear and disappear within hours.

Additional complexity: you need to account for fees on both exchanges, liquidity, and position open/close costs. Without automation this is impossible to track.

Solution: automatic scanner and execution

DeltaZero Arbitrage Finder scans 761+ pairs on 9+ exchanges and calculates:

- Net spread (accounting for fees on both exchanges)

- Composite scoring (liquidity × spread × stability)

- Historical stability (how long the spread persists)

- Auto-execution when yield threshold is exceeded

Net Yield = Funding_A − Funding_B − Fee_A − Fee_B

Example: how it works

On exchange A the funding rate is +0.05% every 8h (longs pay shorts). On exchange B it's -0.02% (shorts receive). Open a long on B, short on A. Price movement is neutralized, and the 0.07% spread every 8 hours is your income.

Expected yield

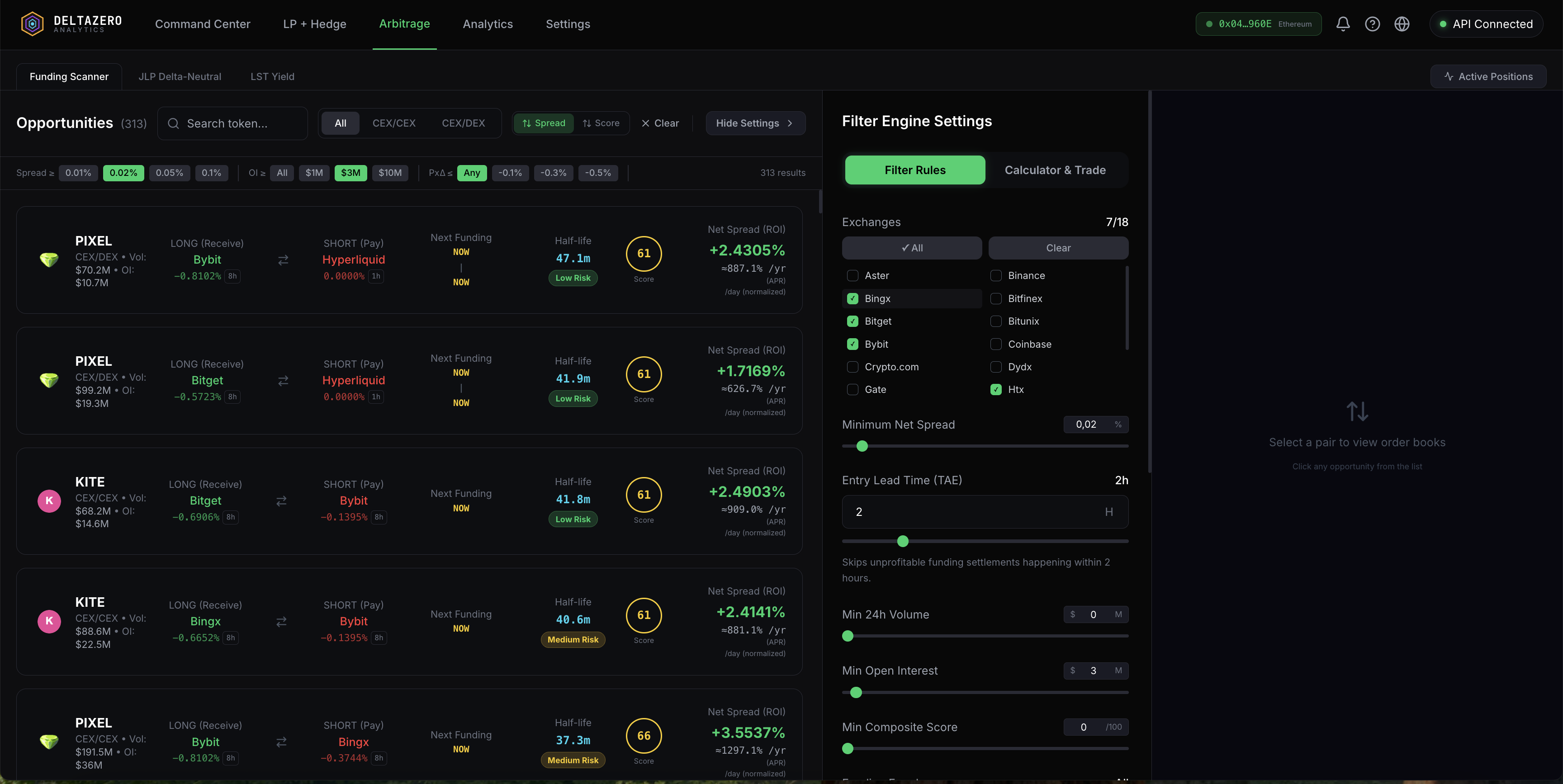

Arbitrage scanner in the terminal

Visualization of all 761+ pairs with filters by net spread, scoring, exchange and liquidity. Found a profitable pair — execute the trade right from the terminal.